Retirement in America: An Analysis of Retirement Preparedness Among Working-Age Americans

Retirement in America: An Analysis of Retirement Preparedness Among Working-Age Americans

This research examines the retirement preparedness of working-age Americans. The research answers key questions relating to retirement savings, access to retirement plans, and how saving for retirement interacts with other financial commitments, such as repaying student loan debt and owning a home.

It also offers a broad examination of how different groups of workers are faring in their preparation for retirement and a consideration of where workers are falling short. The report key findings are detailed below.

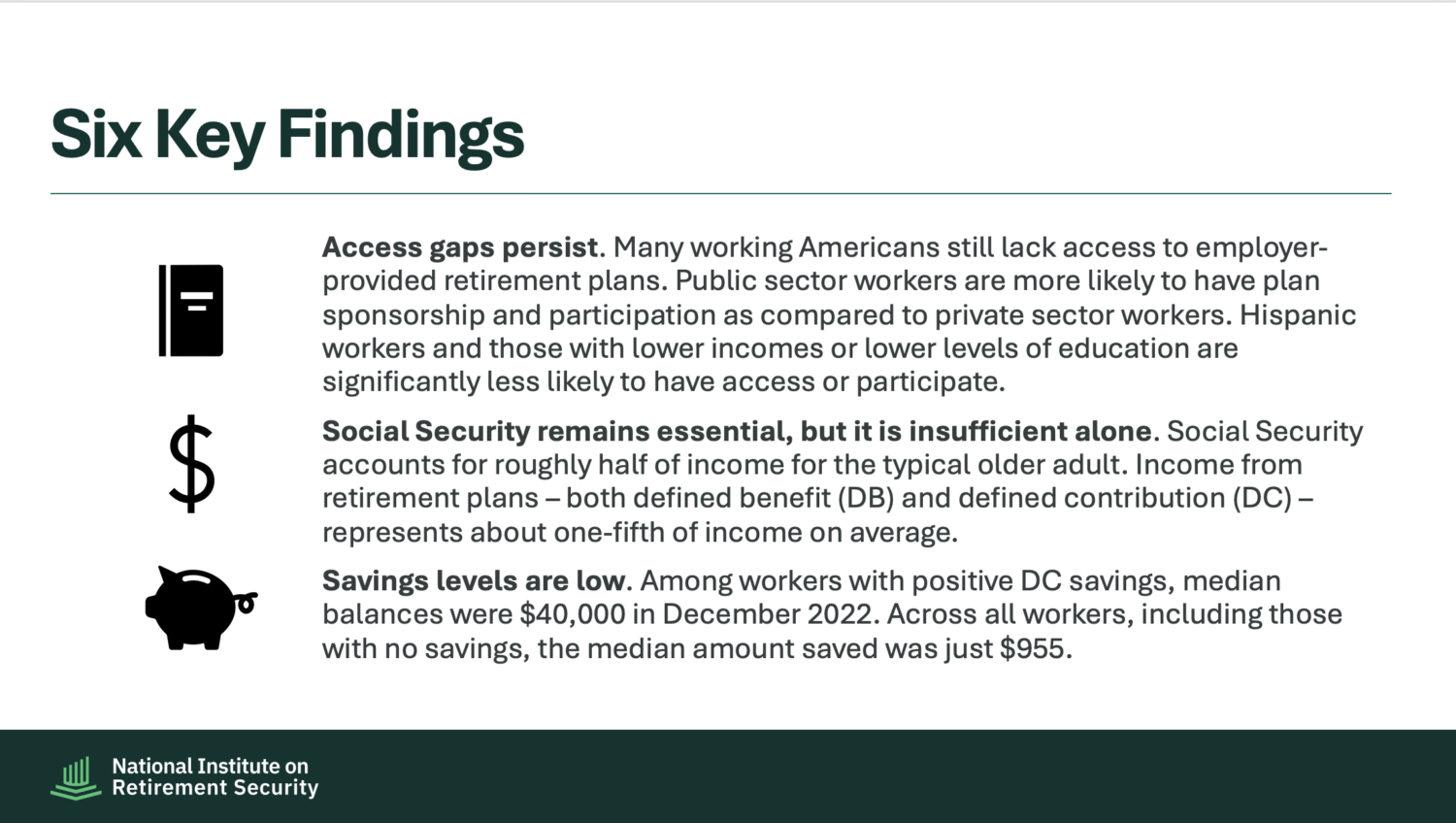

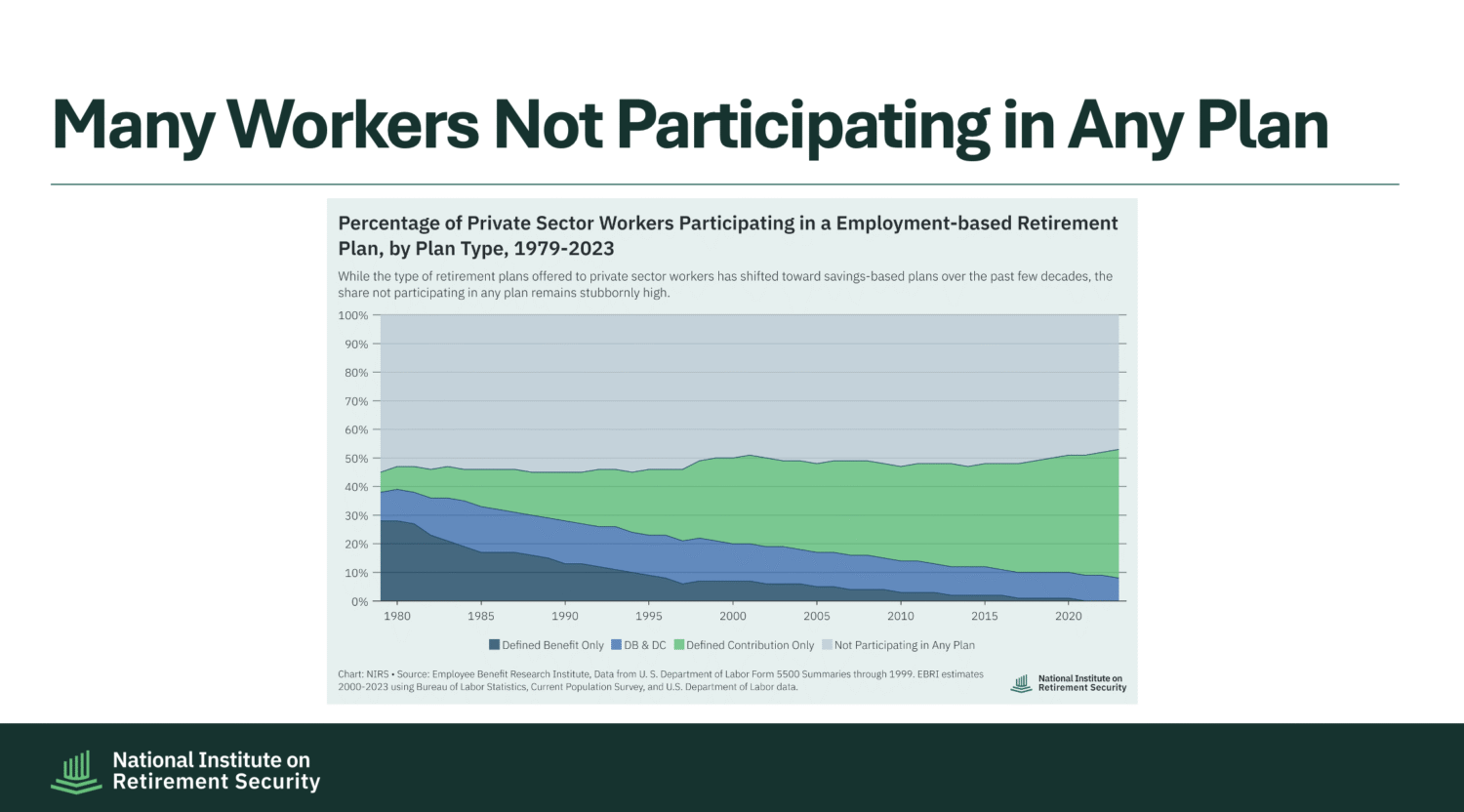

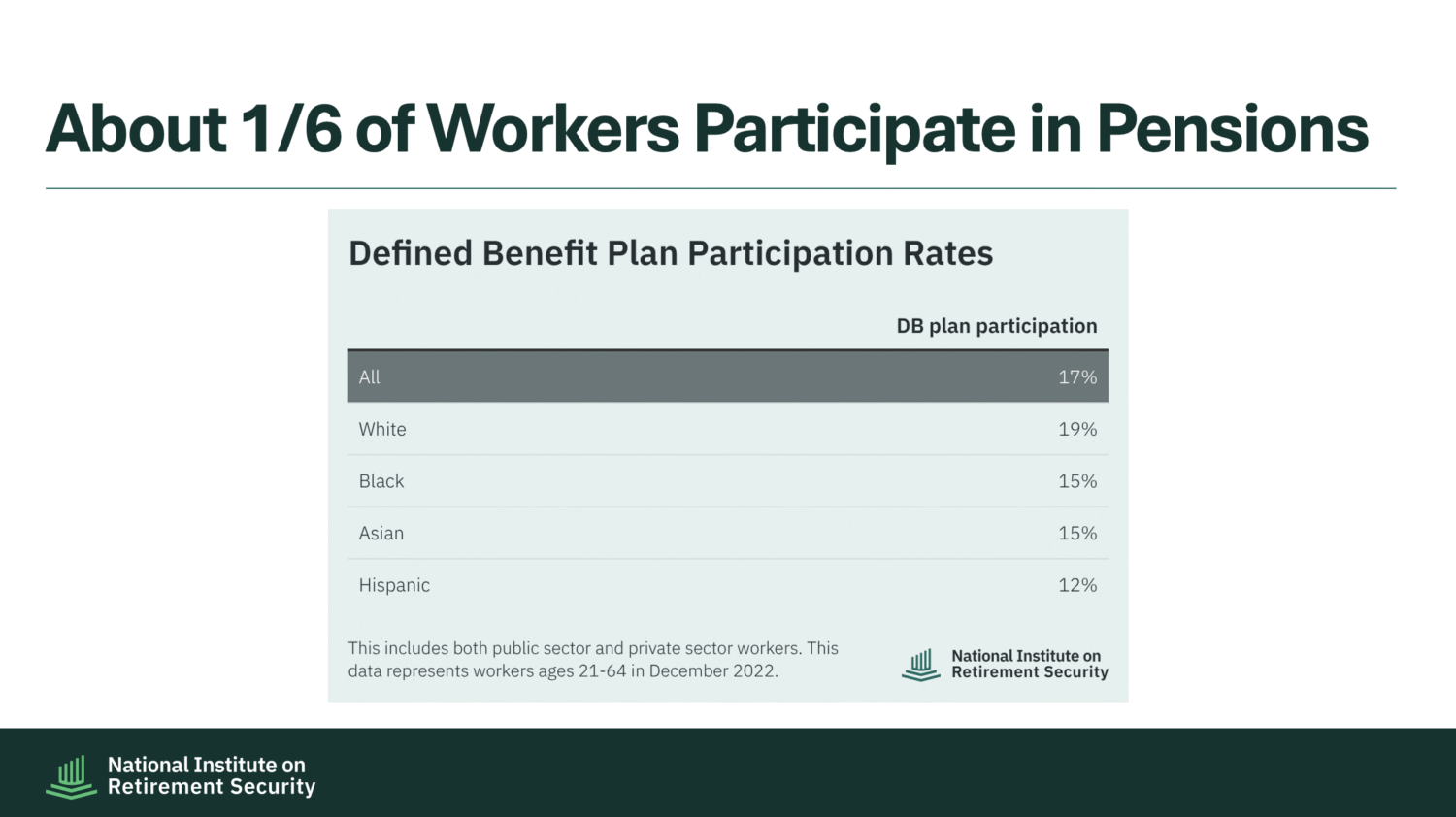

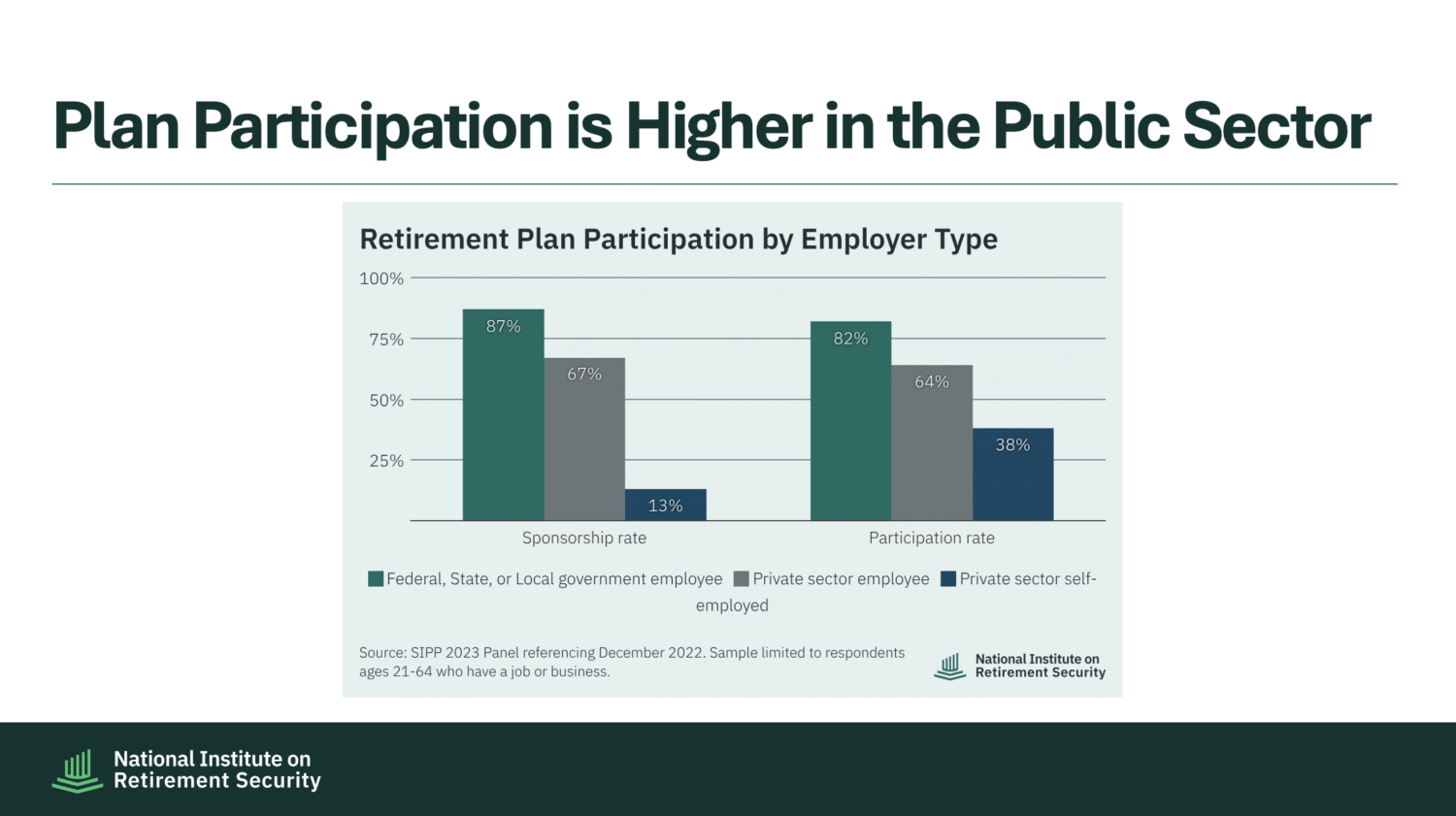

Many working Americans still lack access to employer-provided retirement plans. Public sector employees tend to have higher levels of sponsorship and participation than private sector employees. Hispanic workers and those with lower levels of education and lower incomes tend to have lower rates of both sponsorship and participation.

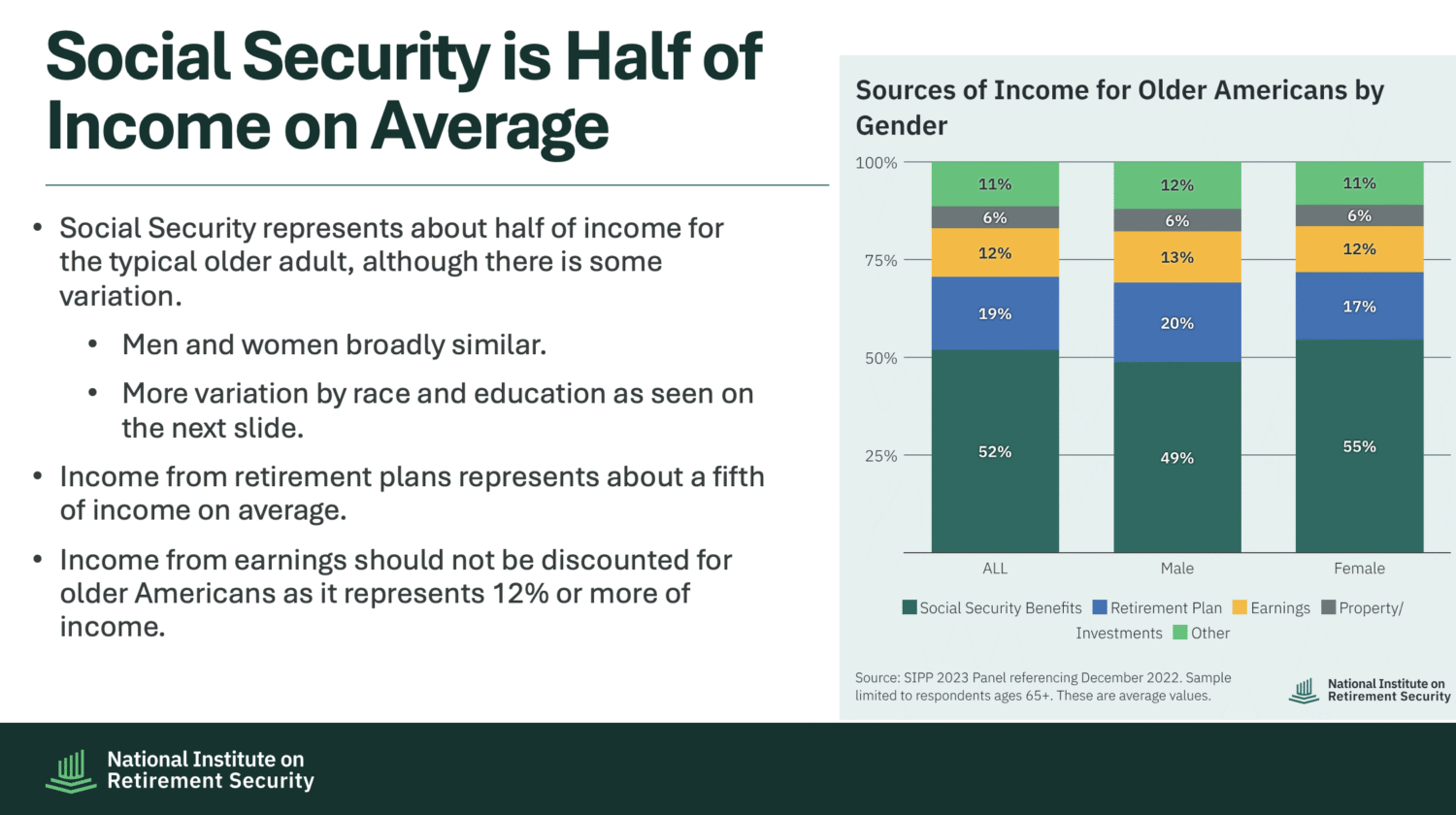

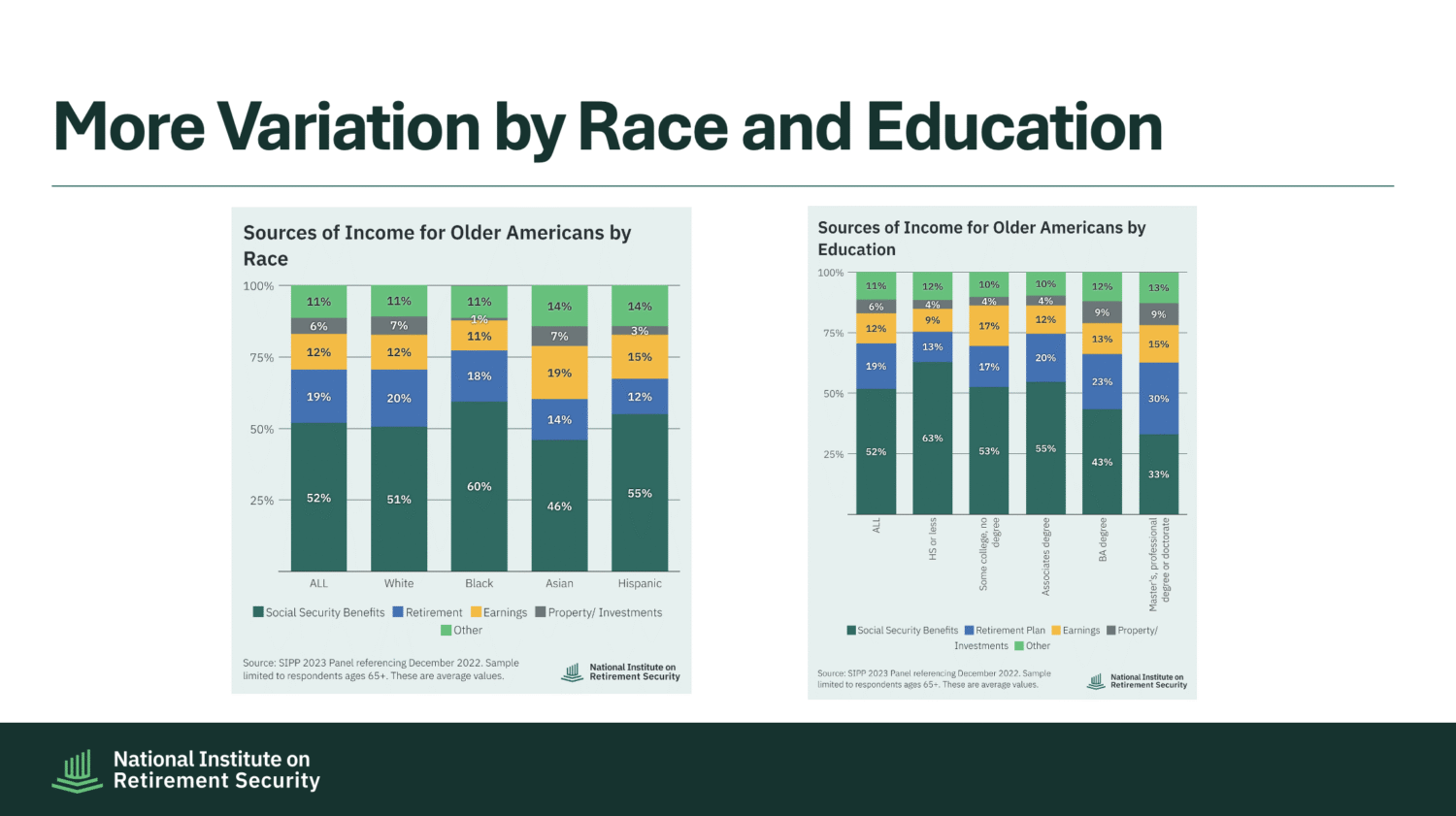

Social Security constitutes half of income for the typical older adult. Income from retirement plans – both defined benefit (DB) and defined contribution (DC) – represents about a fifth of income on average. Income from earnings is also an important income source for many older adults.

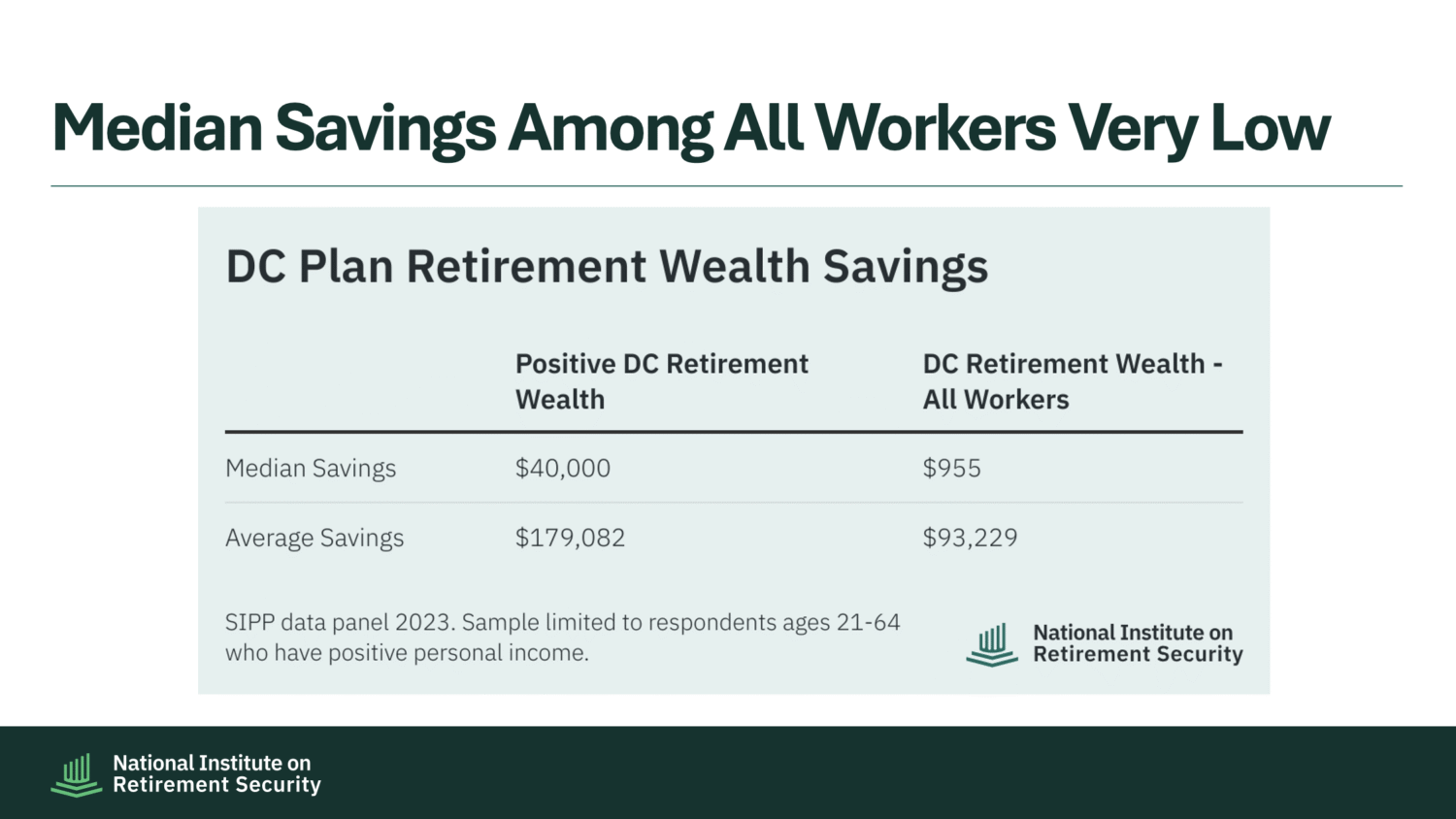

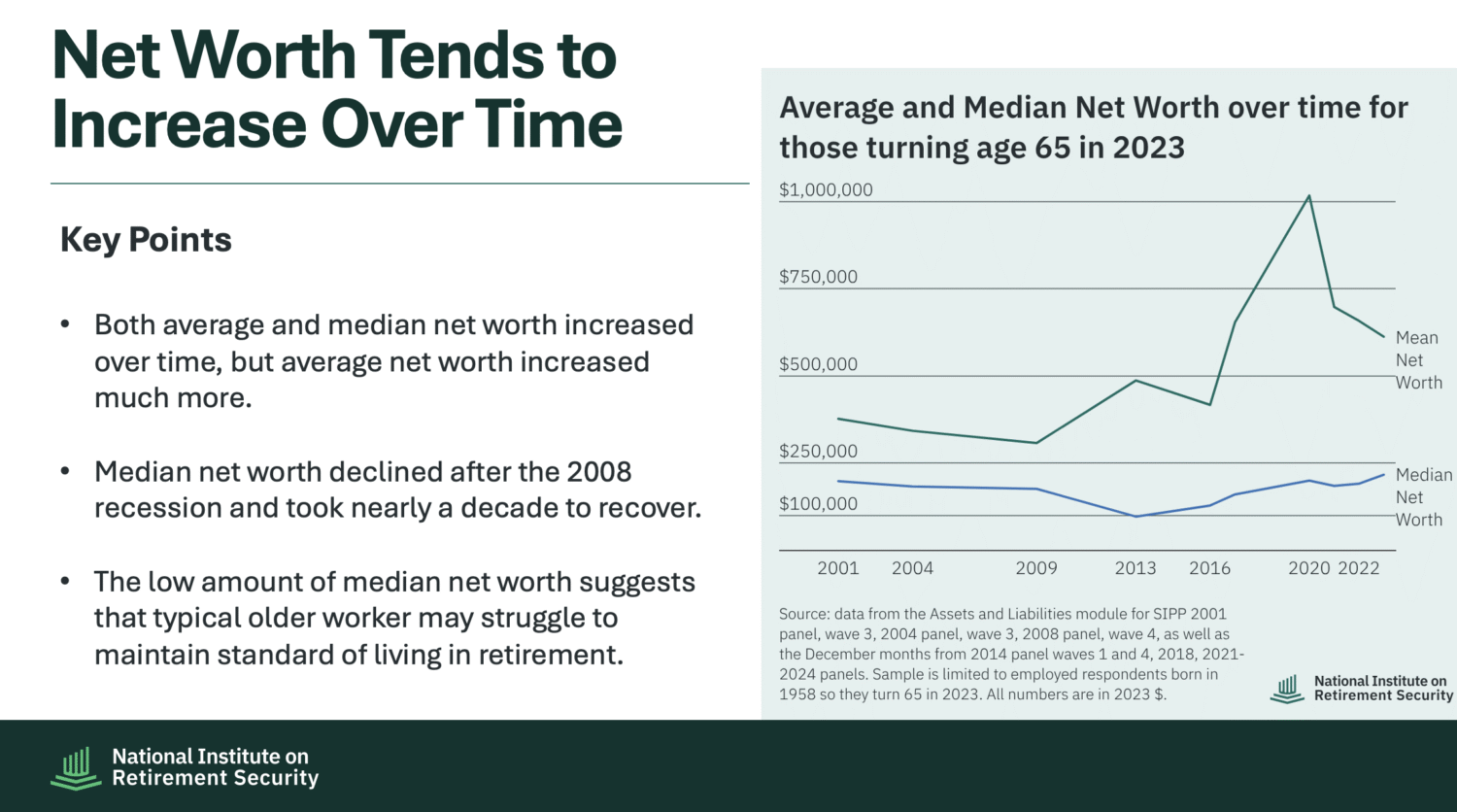

Working individuals who have positive DC savings had median savings of $40,000 in December 2022. Across all workers, including those with no savings, the median amount saved was only $955.

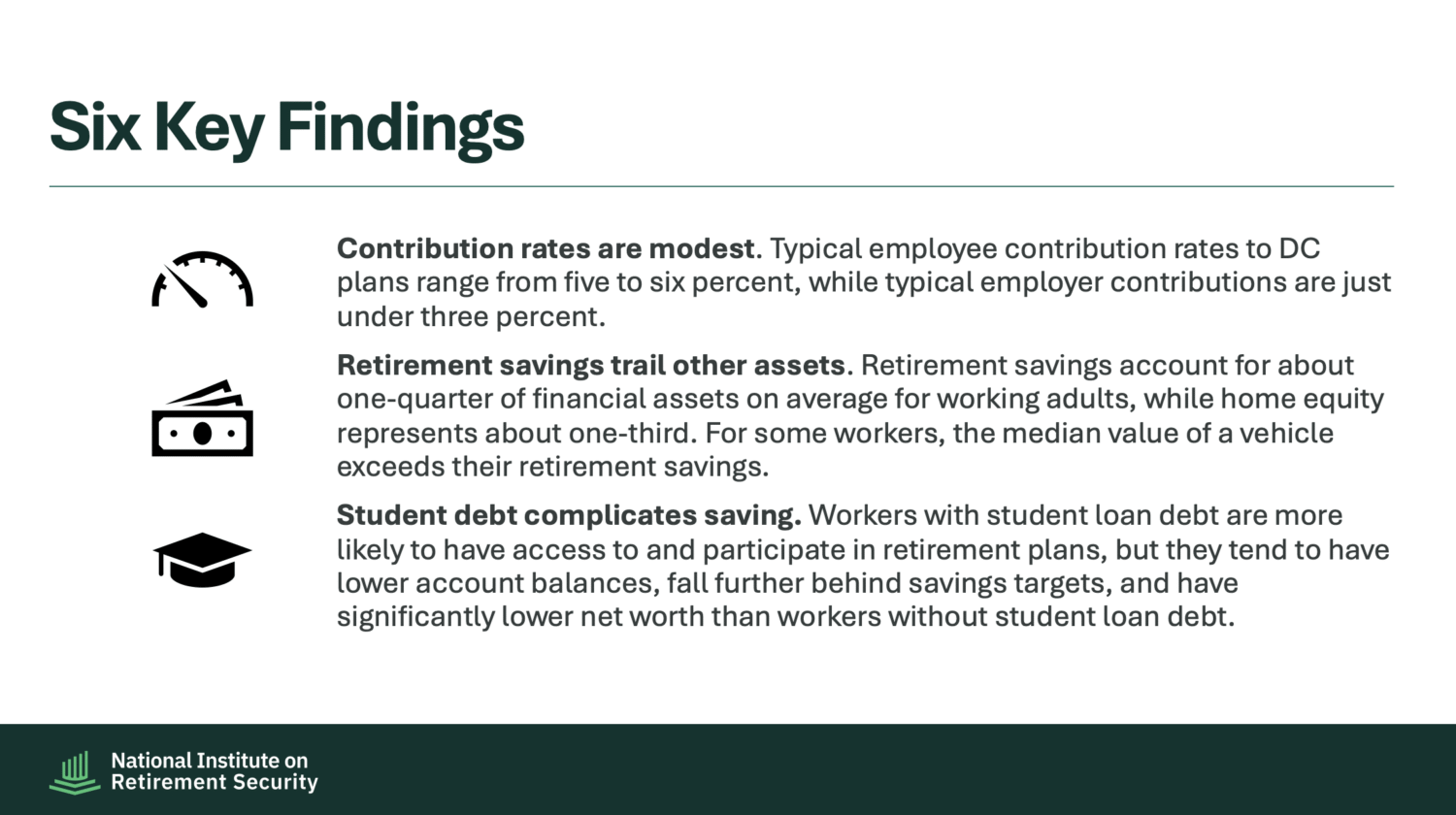

The typical employee contribution rate to a defined contribution savings plan is between five and six percent and the typical employer contribution rate is just under three percent. There is modest variation in contribution rates across different demographic cohorts with employee contributions generally increasing with age, education, and income.

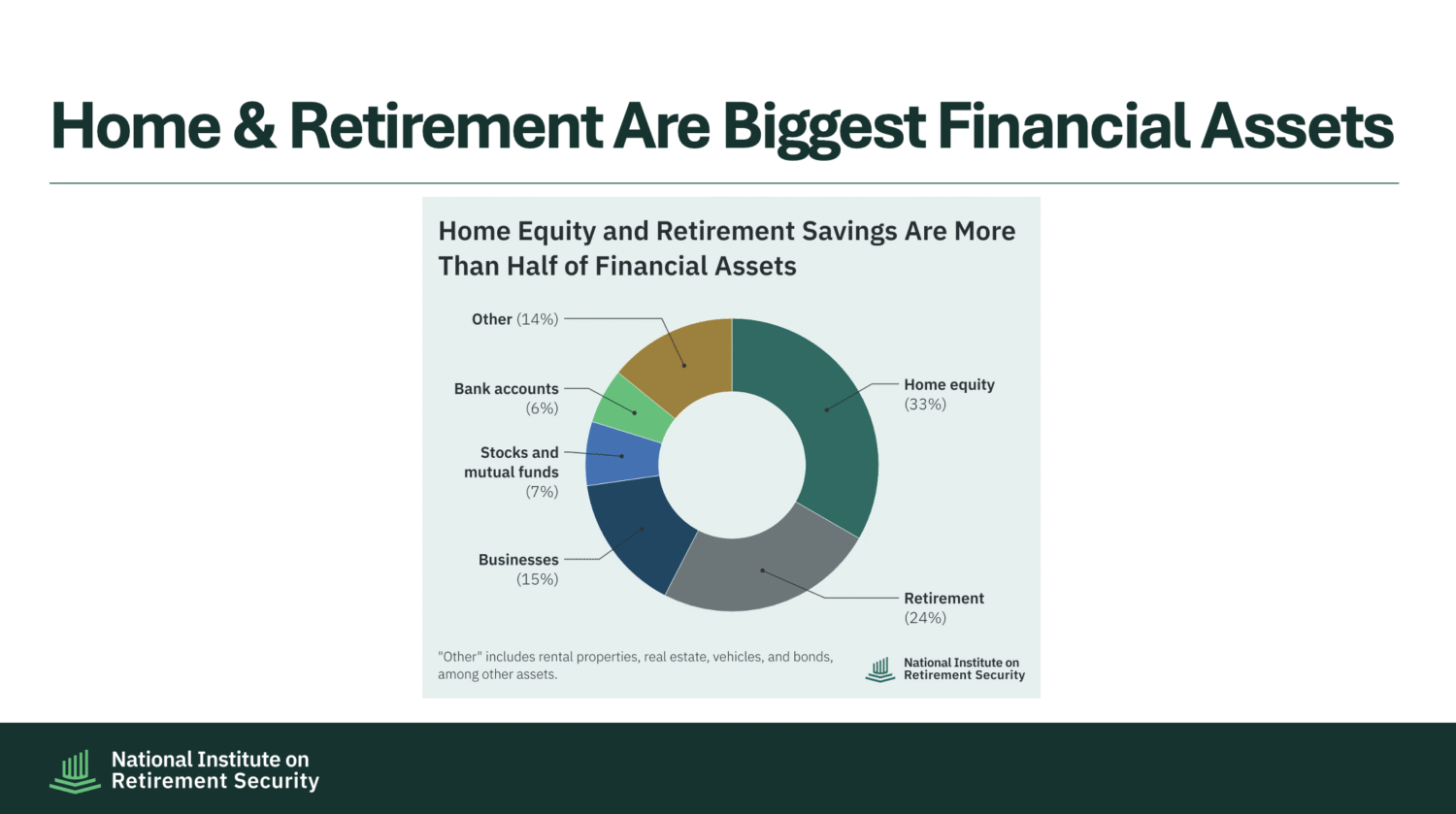

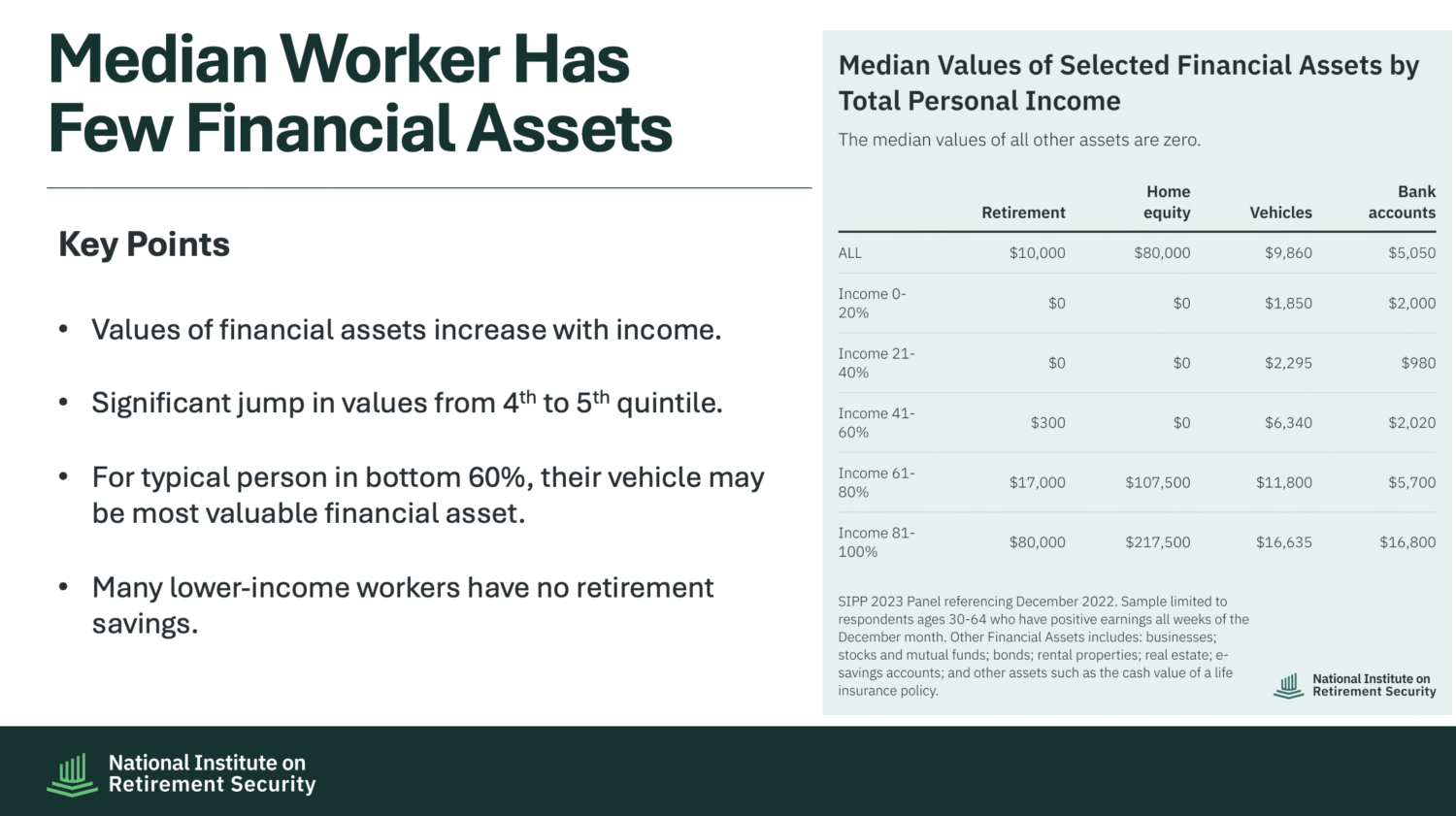

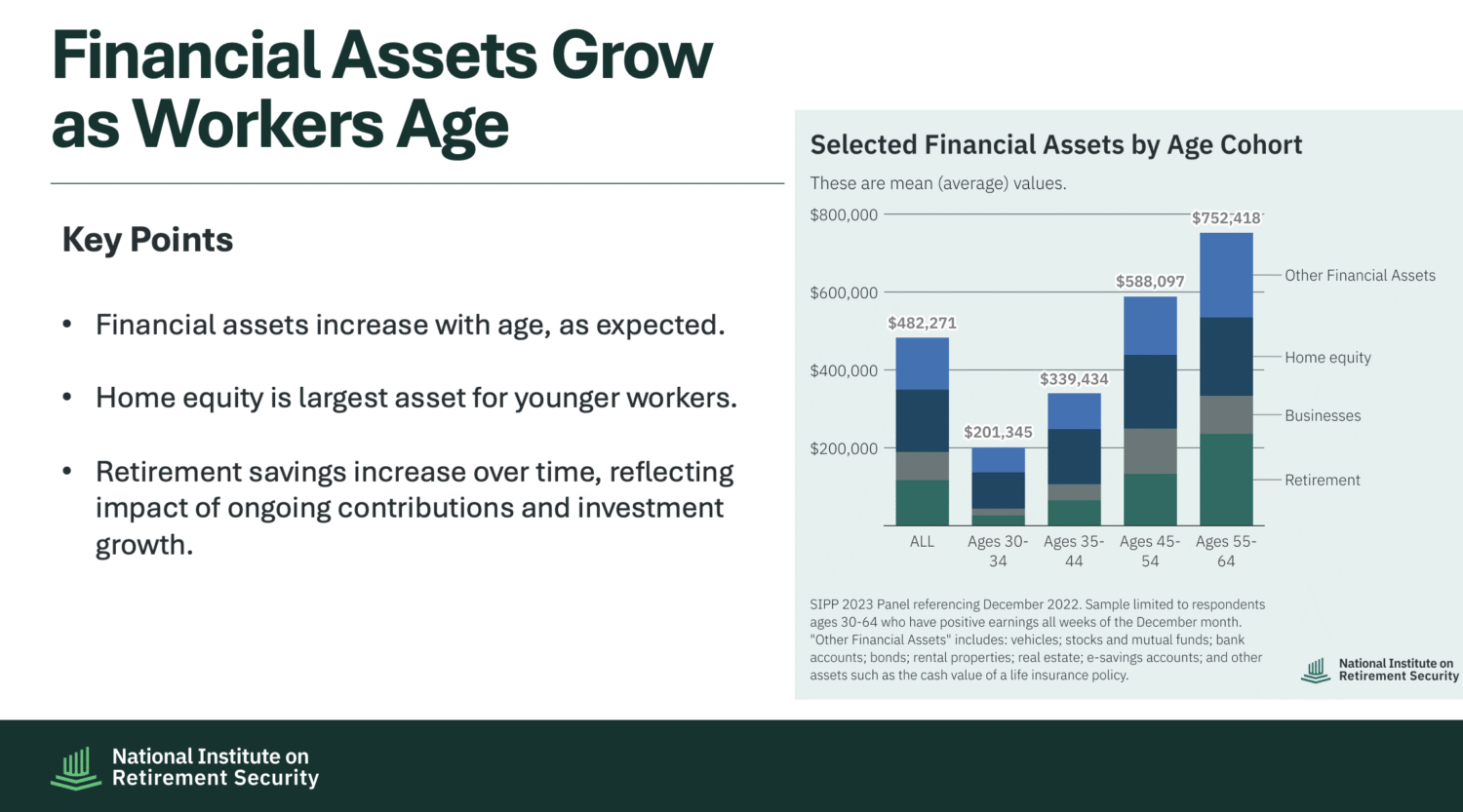

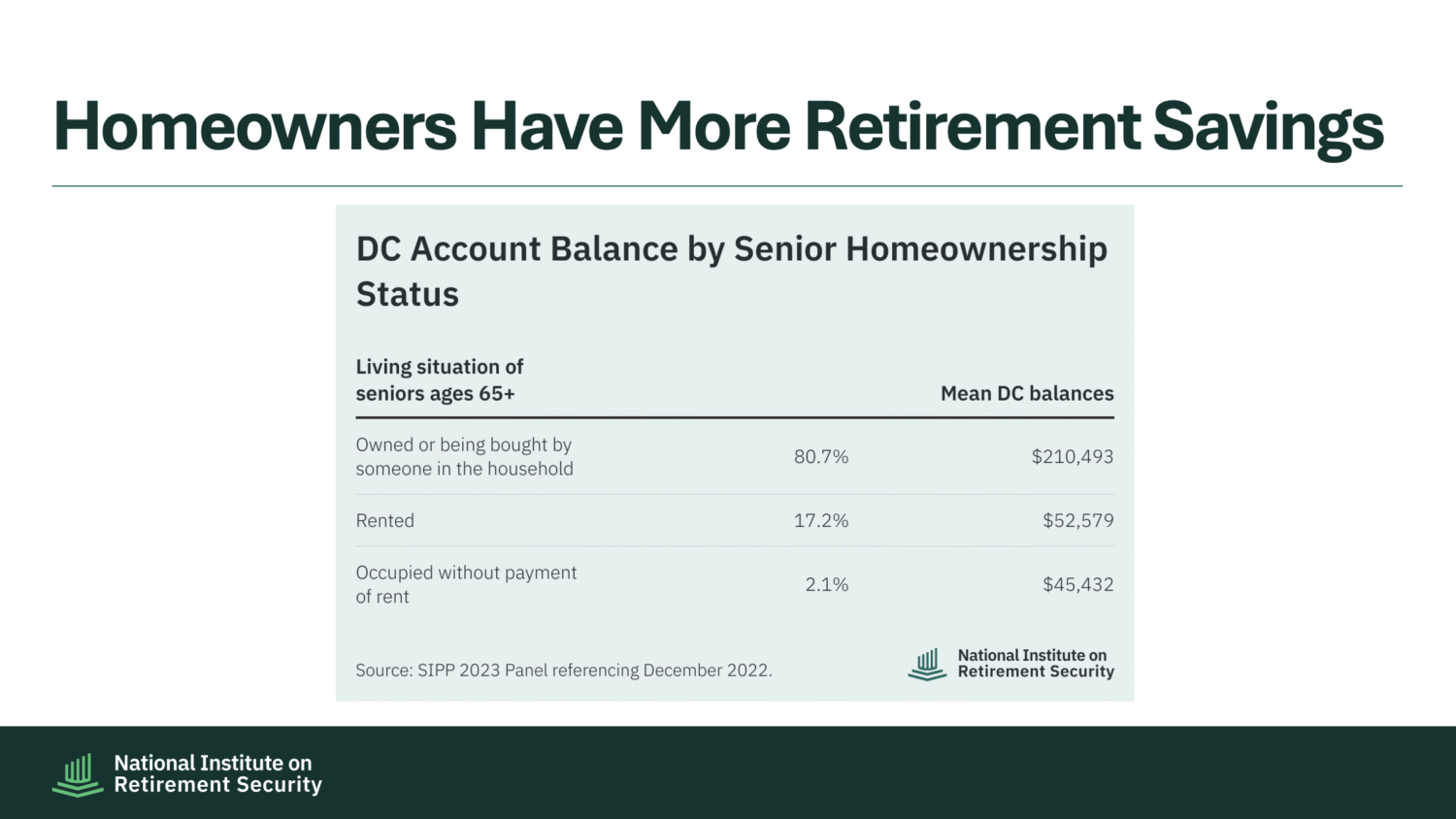

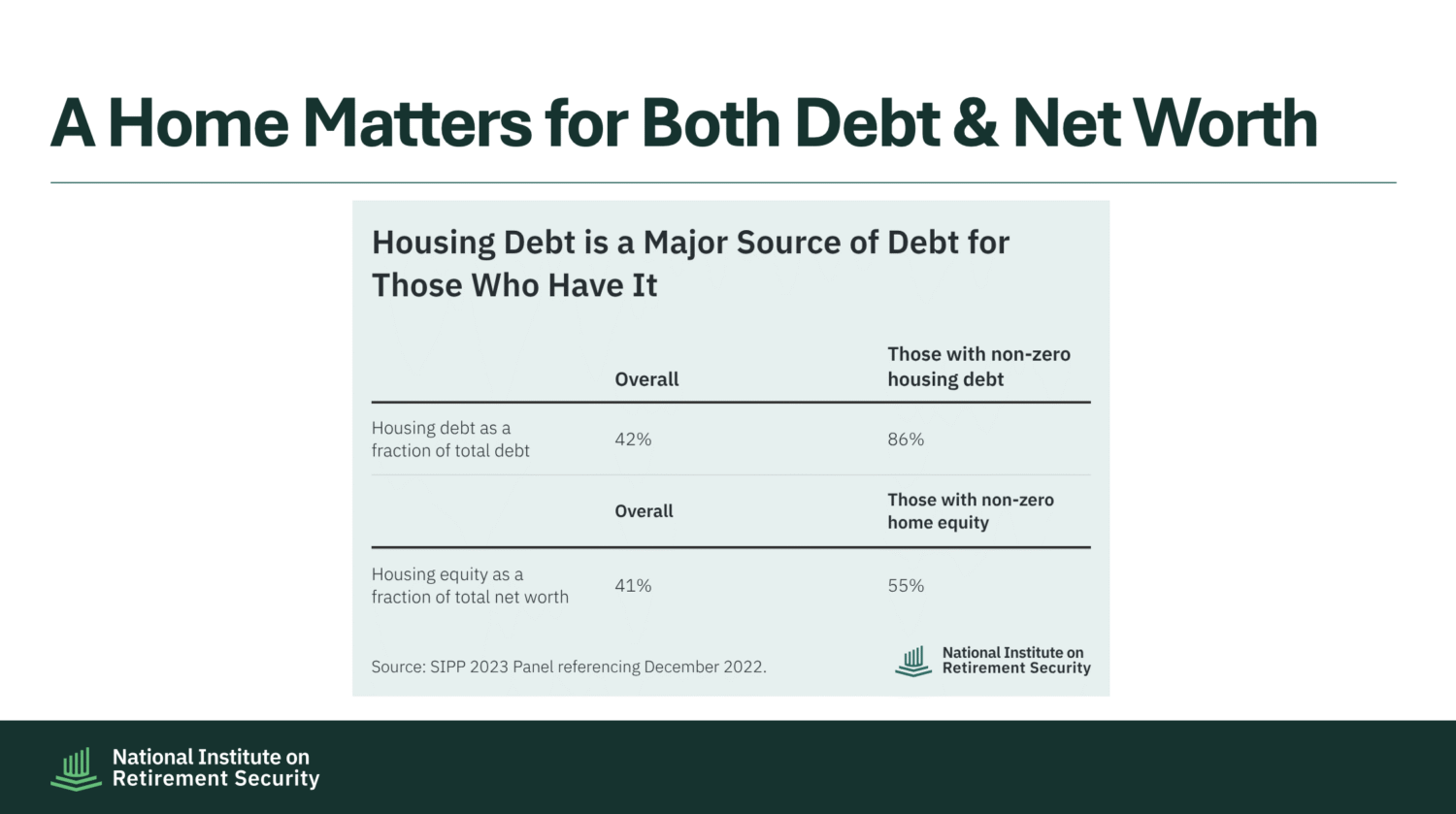

Retirement savings represent about a quarter of financial assets on average for the typical working adult, while home equity represents about a third. For some groups of workers, the median value of a vehicle exceeds the median value of retirement savings.

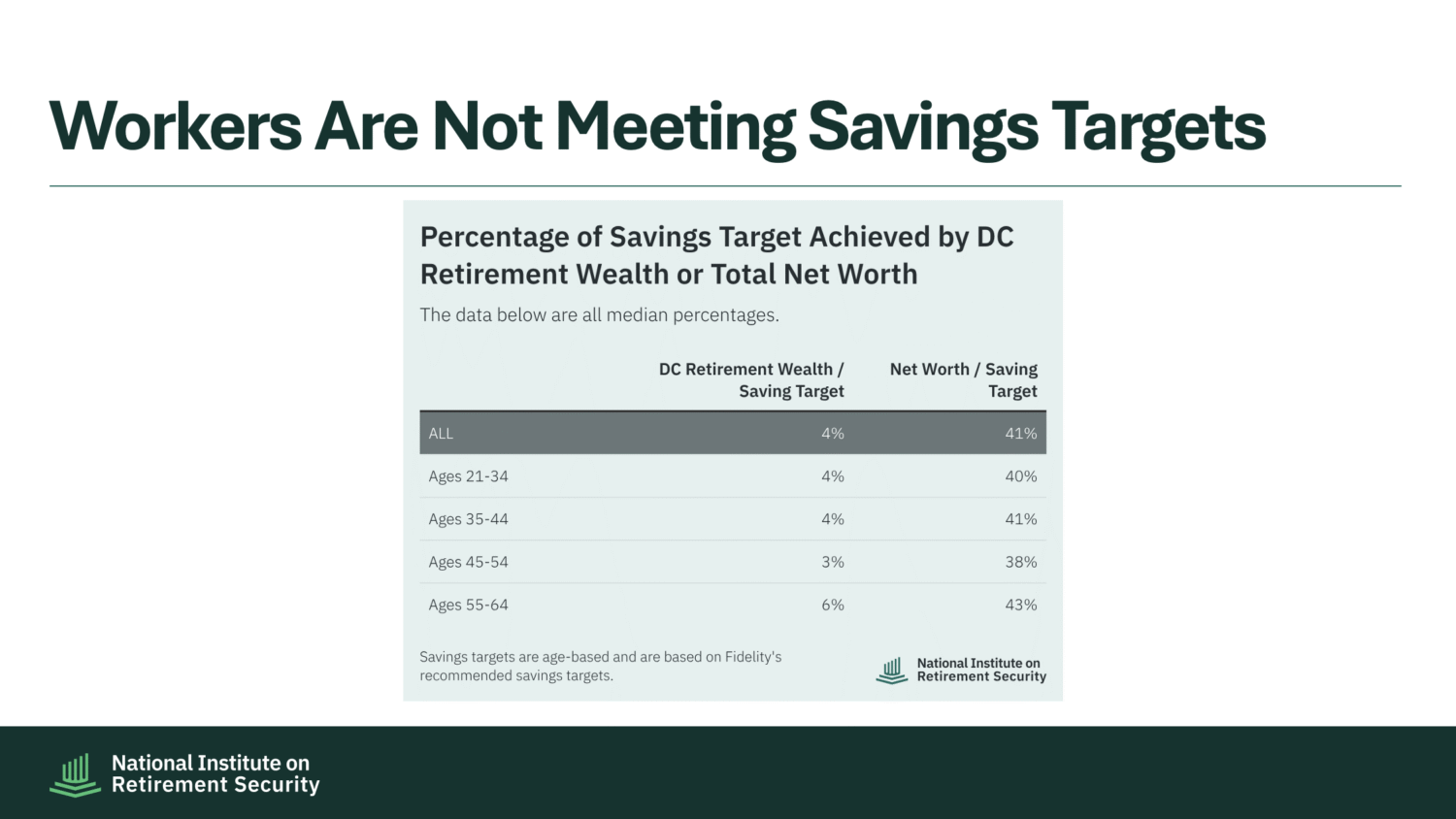

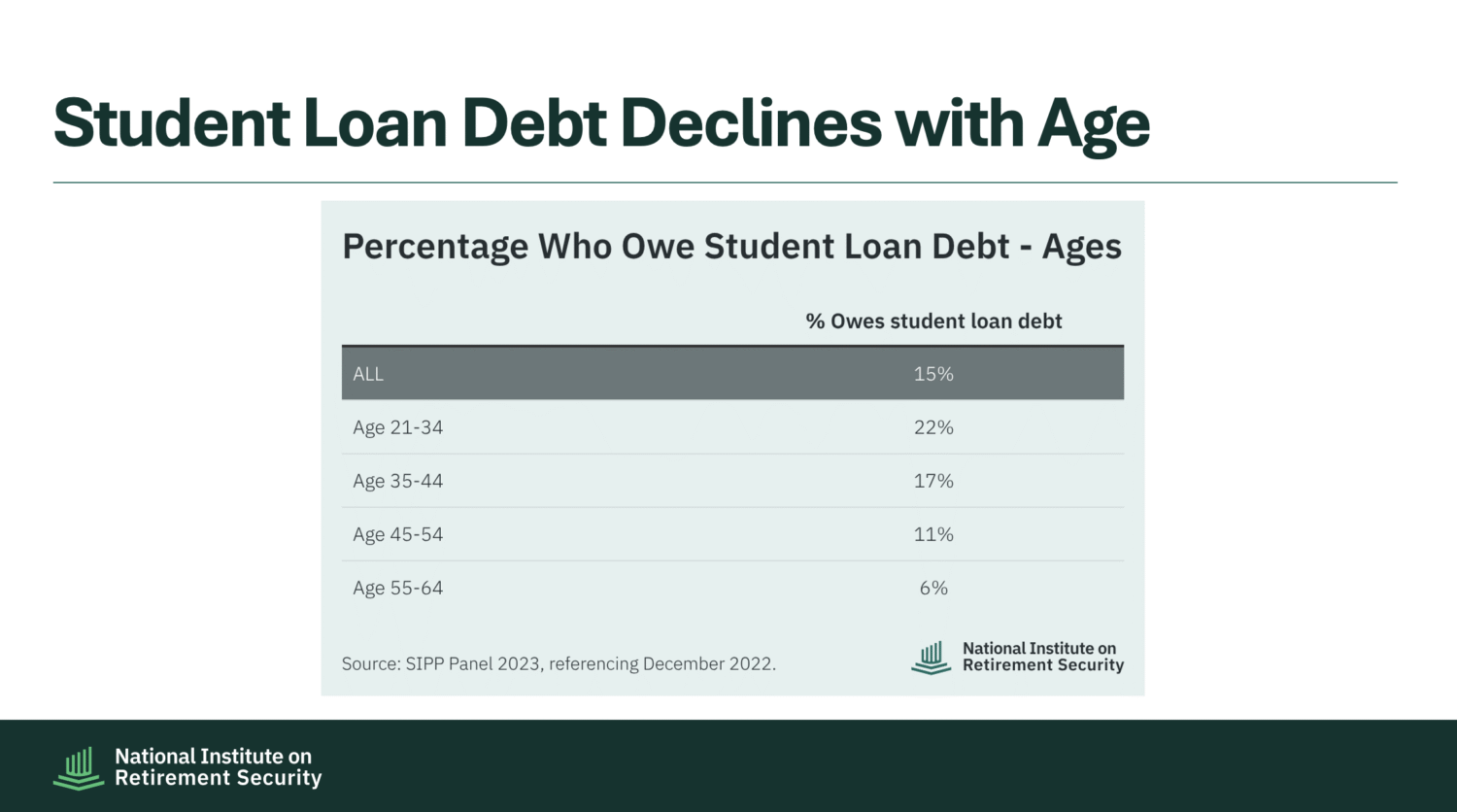

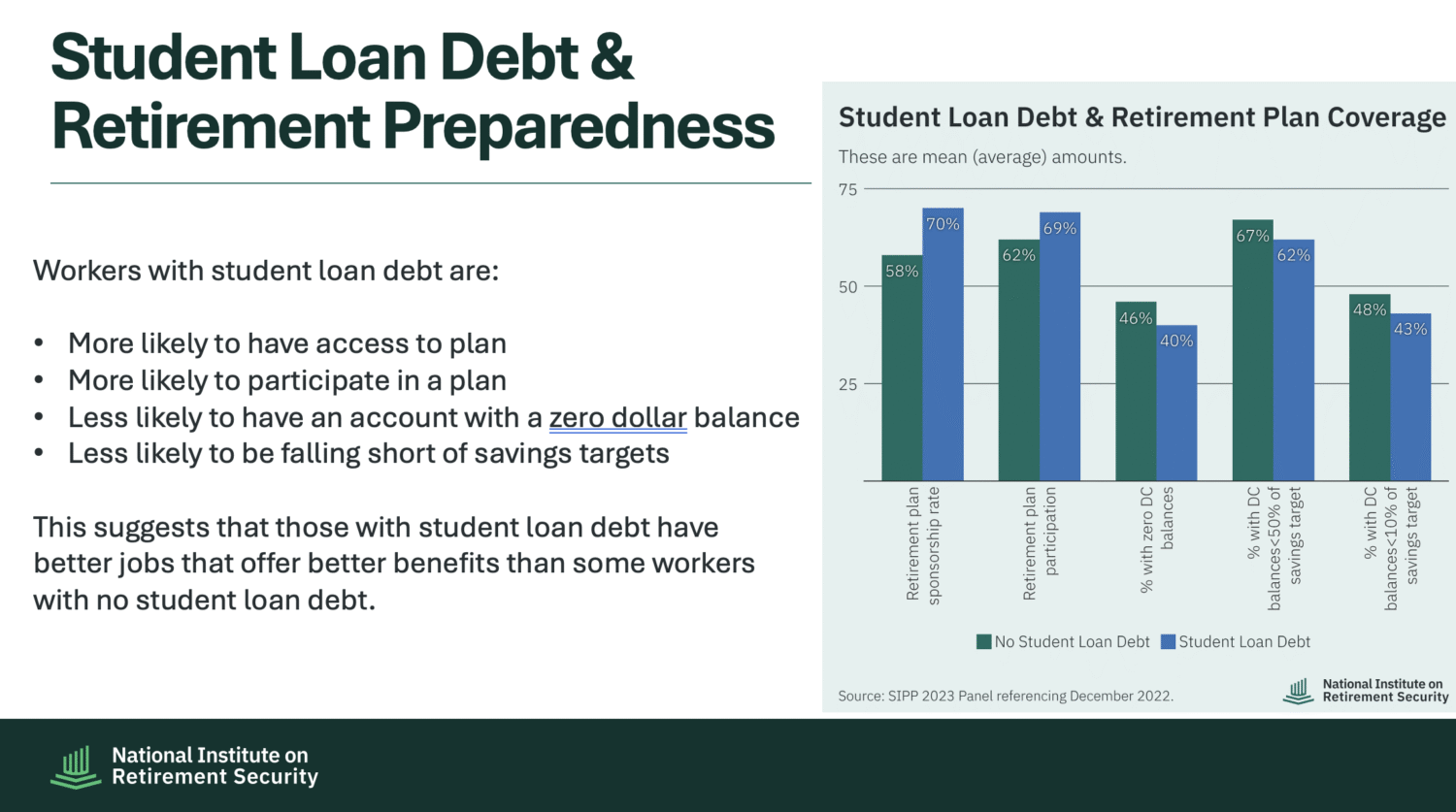

The interaction between student loan debt and retirement savings is complex, but illustrates the tension between different financial commitments. Workers with student loan debt are more likely to have access to a workplace plan, to participate in a plan, and to have a positive balance in their account, but they also have lower account balances, fall further behind in reaching savings targets, and have much lower net worth than those with no student loan debt.

The median amount of retirement savings across the U.S. workforce.

Source: National Institute on Retirement Security | Retirement in America

52%

of retirement income for older Americans is derived from Social Security.

Source: National Institute on Retirement Security | Retirement in America

17%

of U.S. workers had a defined benefit pension plan as of December 2022.

Source: National Institute on Retirement Security | Retirement in America

24%

of seniors have housing debt.

Source: National Institute on Retirement Security | Retirement in America

“At a time when Americans are facing a growing affordability crisis, we need to recognize that retirement should be part of that conversation. Most retirement programs today rely on workers saving voluntarily, with the tension between saving and the cost of buying a home, daycare, and college creating enormous challenges for the middle class. This research shows the fragility of both the nation’s retirement infrastructure and retirement preparedness for the typical U.S. household.”

Policy Ideas for Boosting Defined Benefit Pensions In The Private Sector

In response to a request for information issued by the U.S. Senate Health, Education, Labor, and Pensions (HELP) Committee, the National Institute on Retirement Security has submitted a research issue brief with policy ideas to help expand defined benefit (DB) pension coverage for private-sector employees. The research brief, Policy Ideas for Boosting Defined Benefit Pensions […]

The Forgotten Generation: Generation X Approaches Retirement

Generation X often is referred to as the forgotten generation, sandwiched between the large and culturally powerful Baby Boomer and Millennial generations. Today, Generation X commands less attention than Boomers and Millennials from both researchers and the media. A groundbreaking new report aimed at correcting this oversight, at least in terms of assessing the retirement […]

Stark Inequality: Financial Asset Inequality Undermines Retirement Security

This report finds that economic inequality continues to grow, with Blacks and Hispanics owning only a sliver of financial assets. Even though the Gen X and Millennial generations are more diverse, whites continue to dominate when it comes to accumulating financial assets. This economic inequality ultimately translates into financial insecurity in retirement, which is exacerbated […]

The Missing Middle: How Tax Incentives for Retirement Savings Leave Middle-Class Families Behind

This report documents how current tax incentives fail to promote adequate retirement security for the middle class. It considers the impact of factors including marginal tax rates, retirement plan participation, and income distribution on retirement saving levels. The Missing Middle: How Tax Incentives For Retirement Savings Leave Middle Class Families Behind also offers potential solutions […]