This analysis finds that defined benefit (DB) pension plans offer substantial cost advantages over 401(k)-style defined contribution (DC) accounts. A typical pension has a 49 percent cost advantage as compared to a typical DC account, with the cost advantages stemming from longevity risk pooling, higher investment returns, and optimally balanced investment portfolios.

A Better Bang for the Buck 3.0: Post-Retirement Experience Drives the Pension Cost Advantage is co-authored by Dan Doonan, NIRS executive director, and William Fornia, FSA, Pension Trustee Advisors president.

This report follows two previous analyses conducted in 2008 and 2014 comparing DB plans and DC accounts, and it includes two new elements not included in the previous studies: 1) the impact of the current low interest rate environment; and 2) how saving mid-career rather than early career reduces total retirement savings.

The research’s key findings are as follows:

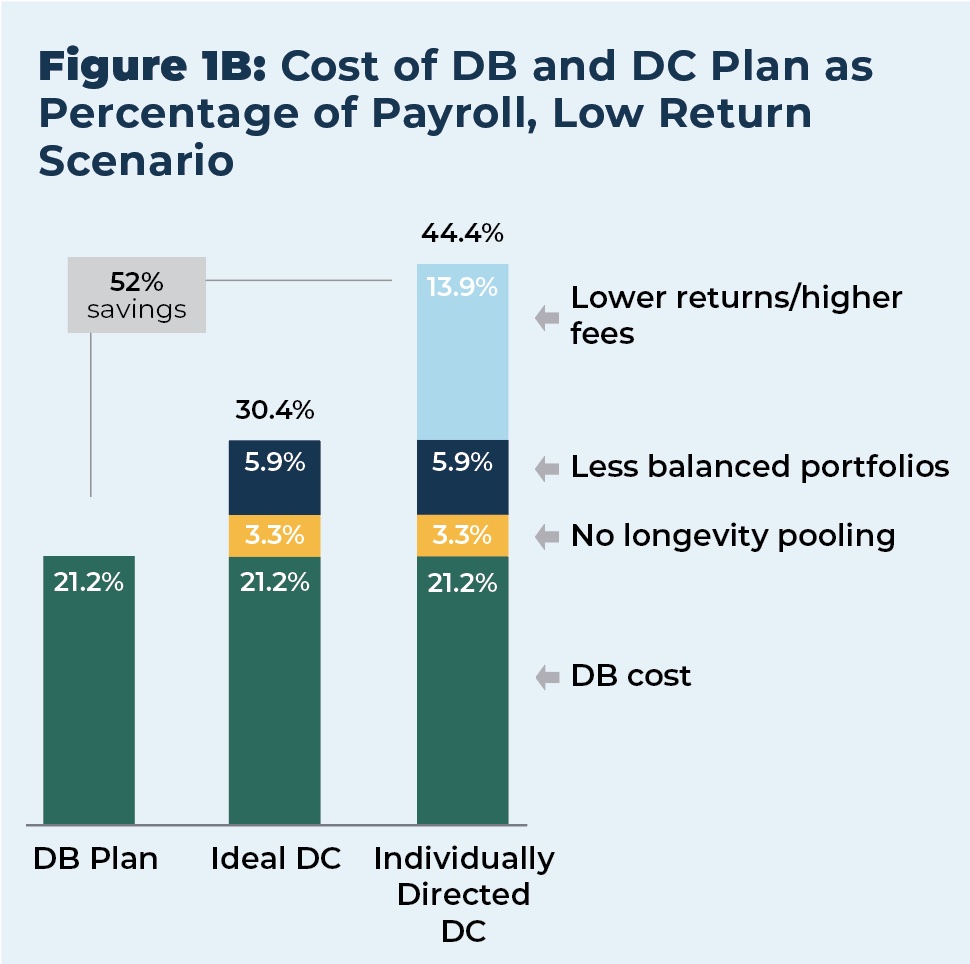

A typical DB plan has a 49 percent cost advantage compared to a typical individually directed DC plan because of longevity risk pooling, asset allocation, low fees and professional management. Longevity risk pooling accounts for seven percent of the cost savings, a more diversified portfolio drives another 12 percent of the cost savings, and superior net investment returns from lower fees and professional asset management generate a 30 percent cost reduction.

A DB pension plan costs 27 percent less than an “ideal” DC plan, with below-average fees and no individual investor deficiencies.

Four-fifths of the difference in costs between the DB plan and an individually directed DC plan occurs during the post-retirement period. Retirees typically move from an environment that benefits from a long investment horizon and fiduciary protections to one where individuals manage their spend-down on a short-term basis without the benefits associated with longevity risk pooling.

This research compares the relative costs of DB plans and DC accounts by constructing a model that first calculates the cost of achieving a target retirement benefit in a typical public sector DB plan. This includes calculating this cost as a level percent of payroll over a career, then calculating the cost of providing the same retirement benefit under two different types of DC plans: an “ideal” DC plan modeled with generous assumptions and a typical individually directed DC plan. Additional details on the methodology that account for the impact of alternative economic and demographic assumptions can be found in the report’s Technical Appendix.

Evolution and Growth: How Public Pension Plans Have Diversified Their Investments Amid Changing Markets

A report from the National Institute on Retirement Security (NIRS) and Aon examines the changes public pension plan investing has undergone throughout the twenty-first century.

Pensionomics 2025: Measuring the Economic Impact of Defined Benefit Pension Expenditures

Pensionomics 2025: Measuring the Economic Impact of Defined Benefit Pension Expenditures finds pending powered by U.S. private and public sector defined benefit pensions contributed significantly to the economy. In 2022, retiree spending of public and private sector pension benefits generated $1.5 trillion in total economic output, supporting 7.1 million jobs across the nation.

In partnership with AARP and NRTA, NIRS has developed a series of state-by-state infographic fact sheets regarding the public employee and teacher retirement systems across the country.

These fact sheets present a snapshot of these retirement systems along with key data from NIRS research and other sources.